A Crude Problem

In an earlier blog, I wrote that the world was on the verge of a major energy crisis. I noted in that blog how much the price of oil had climbed during the period from beginning my research to publication of the blog (around two days). Three days later, the price of oil in early trading on Asian markets had raced above $118/barrel – a rise which for a moment threatened to eclipse the $147/barrel that oil reached in 2008 which caused political panic, global recession and demand destruction. To be honest, I am surprised and puzzled that oil has not continued its vertiginous climb, but has instead hovered around the $100/barrel mark reflecting what I think is a seriously mis-placed optimism bias, which I think considerably under-prices the risk.

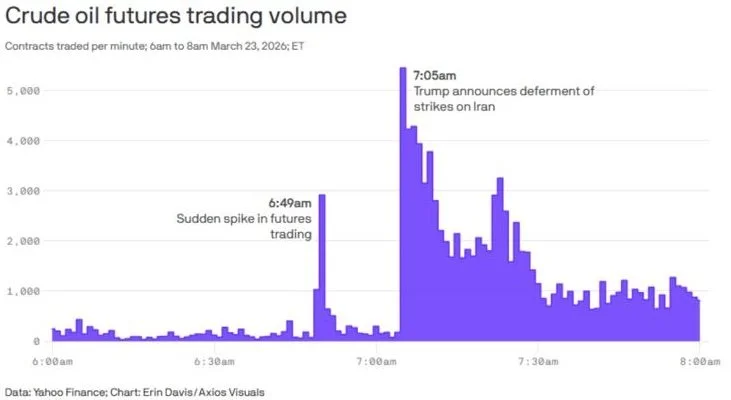

Given the economic, social and political consequences (in that order) of unsustainably high oil prices, it is not surprising that, in order to try and reassure nervous markets, the G7 earlier this month agreed to its largest ever release of strategic oil reserves (400 million barrels) and is apparently considering a second such release. President Trump’s statement on Monday morning that the US would delay bombing Iranian energy and power infrastructure for five days as he was in negotiation with Iran (a claim that has been disputed by the Iranians who have asked somewhat rhetorically whether he is negotiating with himself) represents his own unique approach to calming the oil markets, demonstrating that he is not entirely impervious to the pressures of runaway energy prices.

Leaving aside the fact that five days gives time for US marines and airborne battalions to arrive in theatre; that the five day deadline will expire after the markets close on Friday evening; and that $580 million was bet on oil prices in the 15 minutes before his intervention (bets which I would sincerely hope global regulators will be looking at very closely), the key takeaway is that something is going on here about which we should all be very worried.

When you have luminaries such as the Head of the IEA warning that this oil shock would be worse than those of the 1970’s and Ukraine put together (my emphasis) or Shell’s CEO talking of severe shortages of energy and fuel, then we should recognise there are very good reasons why Trump should be nervous.

This is a crude problem

First, it is worth noting the difference between crude oil and refined products. Essentially, crude is what comes out of the ground. What we use in daily life (for heating, cars, planes, boats, industrial processes etc) is all refined product. Different types of crude require different refinery processes and most refineries are set up to run certain specific types of refinement, rather a broad range.

Next it is worth looking very quickly again at storage. Since the basic building block of the world’s reliance on refined hydrocarbon products is crude oil, I will focus on the figures around crude supply, since that is where the first pain point is. In my previous blog I noted that there are approximately 8.2 billion barrels of oil available in storage around the world. Crude stocks probably make up around half of that figure – but a large proportion of those stocks are inflexible and therefore not available.

A few facts and figures serve to illustrate why supply of crude is now so concerning:

Daily crude oil supplies are around 84 million b/d (the figure of 20 million b/d transiting the Strait of Hormuz includes those products which have already been refined in Gulf countries).

Daily crude demand is around 84 million b/d (making the market extremely tight/finely balanced)

Global sea-borne crude oil transport is around 44 million b/d, of which, Gulf countries (excluding Iran) account for 13.25 million b/d (or just over 30%).

On 1 March, there were approximately 1.25 billion barrels of crude at sea, of which around 270 million barrels was non-Iran Gulf oil (80% of which was bound for Asia).

Asian refineries are around 42% dependent on sea-borne Gulf crude.

Delivery times vary depending on where a tanker is picking up and discharging its cargo, but, as a rough rule of thumb, an empty tanker sitting off the coast of Oman will take between 13-29 days to pick up crude from the Gulf and deliver it to Asia; 28-32 days for Europe; and 12-26 days for Africa.

Asian refineries account for around half of global refined product.

Putting this all together

We are now 26 days into this war.

Refineries have now almost exhausted their existing stocks of crude reserves (they normally hold 3 weeks of stocks).

Between 85-91% of Gulf crude oil on water on 1 March has now been discharged.

Hormuz remains closed – Iran’s offer of partial re-opening today notwithstanding – so there is no more crude heading to Asia from the Gulf to replace the crude which was at sea.

There is significant crude oil storage and the G7 release will help cover the Hormuz shortfall, but refineries are now eating into both storage and the G7 release.

Shortages are now inevitable

Crude storage inventories remain strong and there are other sources of crude - countries such as Mexico, Canada and the US will be able to increase their production in the short-run. However, the impact of the loss of Gulf oil the finely-balanced crude oil market means that demand now exceeds supply - a crunch exacerbated by increasing numbers of countries adopting defensive positions with regards to their crude oil stocks.

Due to the reliance of Asian refineries on crude from the Gulf (and the fact that they are set up to operate on Gulf-quality crude), there is a growing risk that they may run out of crude to refine and be forced to shut down - once a refinery is shut-down, it can take up to two weeks to restart it. Those refineries which do manage to replace Gulf crude will be forced to pay a premium to buy it – which they will pass through to their customers. Since energy is the key input value for most products, this has huge implications for a global economy which relies so heavily on product refined in Asia.

To return to timings. Given the journey lengths from the Gulf to Asia, even if the Strait of Hormuz were to be fully re-opened tomorrow and all Gulf production returned to full capacity at the same time, there would be a hiatus of between two to four weeks during which crude made its way to Asia for refining. There would then be a further two week pause during which Asian refineries were re-started and returned to capacity. But a full re-opening is not going to happen and when it does, it may be months or even years before the Gulf is able to return to full production.

Conclusion

The US/Israeli attack on Iran was not only an unnecessary war of choice, but the absence of planning means that, without wishing to sow panic, shortages of everything from diesel to jet fuel are now inevitable – they are already affecting Asia, Europe will be next. And those shortages will compound the shortages in other sectors that have and will result from the closure of Hormuz (as set out in this blog), shortages which could have devastating effects in Africa (in particular with regards to fertiliser).

Even if Trump declares victory, pulls out and goes home tomorrow, the bigger problem now is that Iran has learnt it can exercise real power by closing off the Hormuz and shut down the global economy. If the regime which has learnt that lesson and demonstrated its power so effectively remains in place, global supply chains and Iran’s Gulf neighbours will be eternally hostage to it. The fact that ‘ownership of Hormuz’ features amongst Iran’s demands in the ‘non-negotiation’ with the US shows clearly that it now believes it has a strong hand to play.

It may be that Netanyahu knew that once Trump had begun down the road of a war with Iran, the only way out was regime change. Whether that was his plan or not, I think Trump, belatedly, has recognised this fact (as set out in this blog) – though I am at a loss as to how he hopes to achieve it. Trump’s talk of negotiations this week sits ill with the news of the mobilisation of the 82nd Airborne and the imminent arrival of the USS Tripoli and three more amphibious assault ships. It seems much more likely that he is playing for time until the reinforcements arrive. Invading Iran seems crazy and there are nowhere near enough US troops in theatre (yet) to even begin to achieve it. Seizing Kharg Island may be feasible, but holding it is likely to just as be difficult and costly as forcing and maintaining a safe naval corridor through the Strait.

It may be that the halfway house is to inflict enough losses (economic, military, political) on Iran to force them to be realistic at the negotiating table. But doing so will take time and whilst that effort is underway, the Strait of Hormuz will remain closed to crude oil tankers and the global shortages of refined products will just get worse and worse. That markets are ‘only’ pricing oil at around $100/barrel seems to be incredibly complacent, bordering on cognitive dissonance. If the analysis above is correct – namely that this conflict will go on for several more weeks or months yet – then the market (and political) bets on its short-term impacts will begin to look more and more out of step with reality.