Impact of the Iran War on Supply Chains

When I was in the Foreign Office, we modelled the impact of impediments to world trade of the closure of the most significant seaborne traffic chokepoints. Along with the Malacca Strait, through which the largest volume of seaborne traffic passes, the nightmare was the closure of the Strait of Hormuz (through which the largest volume of hydrocarbons passes). We assessed that Iran would have to be desperate to shut the Strait as the economic damage it would inflict on itself would be catastrophic (export failure, irritation of neighbouring states, and anger in China – which buys a significant percentage of its imported oil from Iran).

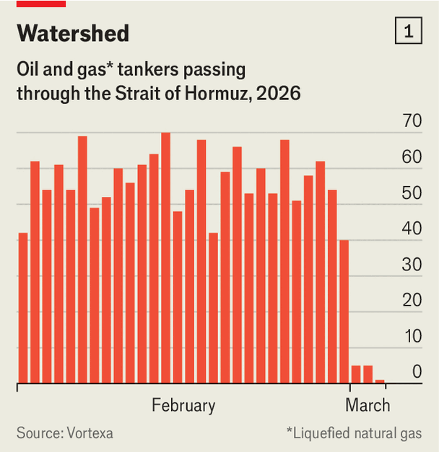

As everyone is now aware, Iran, in response to the US-Israeli assault, has taken that drastic step and closed the Strait of Hormuz to seaborne traffic in an effort to increase global and regional economic pain as a lever (alongside attacks on the energy infrastructure of other Gulf States, including Saudi Arabia’s largest refinery, the world’s biggest LNG-export facility in Qatar, and refineries, fuel tanks and terminals in Kuwait, Oman and the UAE) to put pressure on the US to bring an end to hostilities. The graph below (taken from The Economist) demonstrates just how sudden and total that interruption to traffic has been.

Whilst the main impact has been on oil and gas shipments, with up to 40 super-tankers either waiting to load, or to depart from the Gulf, the closure of the Strait has potential to cause significant disruption to other supply and value chains.

Hydrocarbons

Market reaction to the closure of the Strait had been surprisingly muted. However, today, Brent went through the $90/barrel mark - up from $60/barrel two months ago and gas is now trading at around €55/MWh (up from €27 /MWh on 5 January). Some analysts have suggested gas prices will pass $100/MWh next week if the closure continues: by way of comparison, when Russia invaded Ukraine in 2022, European gas prices hit €310.

Gas

In 2025, more than 80m tonnes of LNG transited the Strait of Hormuz – 75 million tonnes of which came from Qatar’s Ras Laffan complex (17% of global exports). As a result of an Iranian missile strike, production was suspended and force majeure was subsequently declared on gas exports. Returning the facility to full production could take at least a month and there is additional disruption to the global LNG fleet which could add further delays, even if the Strait were to be re-opened tomorrow.

No LNG cargo has crossed the Strait since 2 March, forcing LNG tanker day rates to spike: they were $55,000 (Pacific) or $70,000 (Atlantic) on 5 January; they are now around $300,000. Wood Mackenzie has estimated that global gas supply reduces by around 1.5m tonnes every week that the Strait remains closed.

The availability of gas is particularly worrying for Asian buyers. In 2025, Qatar supplied 30% of China’s LNG imports, 45% of India’s and 99% of Pakistan’s. Even though Europe sources only about 10% of its LNG from Qatar, European prices will inevitably follow Asia’s upwards as buyers begin to compete for the same spot cargoes. In a worrying signal for Europe of the escalating competition from Asian economies to snap up supplies on the spot-market, on 4 March an LNG cargo, bound for France became the first mid-Atlantic cargo to re-route, turning South and heading for Asia.

Following a particularly cold winter, current gas storage in Europe is around 32% of total capacity - below seasonal averages and 10% lower than this time last year (the five-year average is around 45% for this time of year). At current levels of usage, it is projected to fall to around 27% by the end of the month. Europe will seek to aggressively rebuild its storage before next winter, with the aim of reaching 90%, meaning Europe will find itself competing against Asia for gas cargoes against the backdrop of an increasingly tight global market, even after the Strait reopens.

Oil

The oil market is currently well-supplied, with good inventory stocks and a relatively large amount of oil in transit on super-tankers. However, the longer the Strait remains closed, the tighter the oil market will also become.

On a normal day, 14m barrels of crude and 4m barrels of refined products pass through the Strait. Whilst there is some potential to re-route tanker-borne products via UAE and Saudi pipelines, even at maximum capacity, those pipelines can only take a quarter of the crude volumes normally transported by sea. This problem has now become acute. By some estimates, Iraq ran out of storage capacity earlier today and Kuwait will reach the same point over the weekend. If the Strait does not re-open, the UAE will face the same problem by the end of next week and we may begin to see a slow-down in some Saudi production beyond next weekend, despite Saudi capacity to export some of its oil through its land-based pipelines. If the shut-ins are carried out in an orderly fashion and are brief, a field can normally be brought back online within a fortnight. But the longer the shut-in continues and the older the well, the longer it will take to bring them back on-line.

The fact that Asian buyers are already looking for alternative supplies from West Africa, America, Brazil, Guyana and Norway demonstrates the level of global nervousness about supply – and this is likely to begin to drive prices up more aggressively over the coming days. With Brent now trading at over $90/barrel it seems entirely credible that the price will go past $100/ barrel by the end of next week. Another two weeks beyond that could see oil reach record highs of $150/barrel.

Whilst there is some potential to bring new supply online from other parts of the world, even if every well produced to its maximum capacity, it would take six months and only bring 1m-2m b/d to market. US shale drillers, who could potentially deliver a big rise in output, are likely to resist pressure to embark on expensive new drilling programmes until they are certain that higher oil prices would last long enough to cover their additional drilling costs.

The impact of the closure of the Strait can be seen in the premium that Brent already now commands over oil traded in Dubai. And the impact on refined products is even more remarkable. Diesel spreads (the margins refiners earn when turning crude into finished fuel) have gone from $21/barrel to $44/barrel. China has a stockpile of oil equivalent to approximately 140 days’ demand, but does not have the same strength and depth in refined products, and has already halted their export.

Impact on Inflation and GDP Growth

The IMF calculates that a 10% increase in the price of a barrel of oil reduces global GDP growth by 0.15% and increases inflation by 0.4% the following year. This has a particularly noticeable impact on poorer countries for whom energy costs take up a larger share of national expenditure. India (with only 20-25 days of usable oil stock in reserve) is particularly exposed, spending around 3% of GDP on foreign oil a year (it is note-worthy that Trump relaxed his ban on India buying Russian oil this morning). In less developed countries, since more expensive oil costs are not passed through to customers who cannot afford the higher prices, those costs tend to widen fiscal deficits, as state-owned refineries operate at a loss and governments subsidise public consumption.

In Europe, any price increase will be passed straight through to the consumer. European Central Bank calculations suggest that a 10% increase in oil prices adds 0.6% to inflation over three years. And it is not just consumers who will feel the pinch – higher energy costs will also reduce industrial margins, potentially reviving coal demand (see below).

The US will feel less pain – though it does not escape from the impact of the closure of the Strait. The US domestic gas market has limited export capacity, which, because it weakens the connection to global prices, means that energy only constitutes a small element of the US consumption basket and domestic gas prices have so far only increased by 4% since the beginning of the month. Petrol-pump prices on the other hand, have risen by 11% this month alone, posing political problems for a Trump administration that pledged to bring them down. It is not clear to what extent the US Government can and will open the spigots on the 415m barrels in its Strategic Petroleum Reserve.

Impact of the Iran War on Other Products

Coal

Coal prices have jumped 26% reaching $133 per tonne, with similar increases across the Australian and Asian markets (their highest price in more than two years), as utilities and power companies in Europe and north-east Asia respond to perceived gas shortages by substituting coal for gas. By way of comparison, coal prices reached more than $400 a tonne following the Russian invasion of Ukraine.

Aluminium

The Gulf produces around 10% of the world’s aluminium, with major smelters in Bahrain, Qatar and the United Arab Emirates benefitting from cheap access to plentiful hydrocarbon power. US-Israeli attacks on Iran have caused smelter closures and “force majeure” declarations across the aluminium industry in the Gulf, threatening a supply crunch with global stocks already close to historic lows. Bahrain’s Alba smelter, which ranks among the largest in the world and produced 1.6mn tonnes of aluminium last year, declared force majeure on Wednesday. Once the furnaces and smelters are powered down, it can take 6-12 months for a full re-start. Prices on the London Metal Exchange are already at their highest since 2022 at $3,322/tonne. Analysts have suggested they could rise to $4,000 if the closures continue.

Fertiliser

Hydrocarbon gas comprises between 60% and 80% of the production cost of nitrogen-based fertiliser, so the Gulf is unsurprisingly the location of some of the world’s largest fertiliser factory sites. Around one-third of the global trade in urea, ammonia and nitrogen (vital raw materials for the manufacture of fertiliser) passes through the Strait, with Saudi Arabia and Iran being respectively the third and fourth largest global exporters of urea. This makes the Strait of Hormuz the single most critical maritime chokepoint for nitrogen fertilizer trade.

As with oil and gas, no shipment of fertiliser or its raw materials has passed through the Strait since 2 March. In response, the benchmark Egyptian urea price has risen by more than 25% in a week - $625 (£467) a metric tonne today, up from $484 the week before.

In the Northern hemisphere, we are entering planting season, so farmers have the fertiliser they need for this year’s crops. However, this is also the time when farmers begin buying fertiliser for next year: if fertiliser production is curtailed now, it will impact next year’s harvest. With around 50% of global food production dependent on synthetic nitrogen-based fertiliser, there is growing concern about crop production and food security. If crop yields fall, resulting shortages will push up prices for staples such bread, pasta and potatoes, and make animal feed more costly. The impact of those price rises will be felt most acutely in the Global South.

Semi-Conductors

It may seem odd that the closure of the Hormuz Straits should impact the production of semi-conductor chips when the Gulf is so far from their production sites. However, higher input energy prices will impact the viability of the production of semi-conductors. In addition, many vital semi-conductor precursor chemicals are made from oil and gas. And global supply chains risk becoming constrained (as they were during Covid) by cargo ships being empty and/or on the wrong side of the Strait.

Heating Oil

The BBC has reported that some suppliers of heating oil in Northern Ireland (where almost two-thirds of homes use oil for heating), have increased prices by more than 30% since last weekend – from £300 for 500 litres to £425. Whilst this is currently just a problem which has been reported for N Ireland, it is likely to be a much wider problem (I am just about to go downstairs and turn our oil-fired boiler off!)

Airline tickets

The price of flights between Europe and Asia have jumped since the closure of large Middle East hubs has led to thousands of flights being cancelled. Stranded passengers (both those already in the Gulf and those who were due to transit through the Gulf back to Europe and America) who have tried switching to other carriers and routes have encountered higher fares and limited availability.

Groceries

International container transport is highly integrated and tightly balanced. Major container ships circle the world in loops. Containers and ships stuck on the wrong side of the Hormuz Strait will result in gaps appearing in scheduling in other parts of the world. This creates a potential double impact on supermarket bills – cost of shipping (oil price rise) and availability of shipping (containers in the wrong place). Grain prices have already seen a rise in response to increased sensitivity to market constraints in the grain, shipping and oil sectors. If shipping companies choose to avoid the Red Sea/Gulf, then the cost of Asian products is likely to rise as containers take the longer route to Europe. The absence of Iranian exports of pistachio, walnuts, almonds, saffron and dates will drive up their global prices.

Maritime insurance

Leading maritime insurers cancelled war risk cover for vessels operating in the Gulf on Thursday, even though it may be reinstated at new terms. Marine insurance rates could rise by up to 100%, from 0.25% to 0.5% or 1% of the value of the insured asset.

Geopolitics

I know this blog is about the impact of the closure of the Strait of Hormuz on products and supply chains, but I could not resist including a note on the geopolitical impacts of an energy supply crunch.

A more pro-Western Iran or an Iran plunged into longer-term chaos would bring the Russia/China relationship even closer. With China facing a hydrocarbon supply crunch, the obvious place to turn for relief is to Russia. China’s state oil group CNPC announced plans earlier this week to restart a mothballed oil refinery in north-eastern China to handle increased Russian crude imports.

China is also likely to focus on accelerated development of the Power of Siberia 2 Pipeline, designed to supply natural gas from north-west Russia through Mongolia and into China. The absence of Iranian oil is also likely to create a greater premium for China on access to Arctic trading routes to enable a faster and cheaper way to increase volumes from Russia – suggesting that the Greenland saga may resurface in the near future.

However, since Russia already accounts for 20% of China’s crude imports, adding Iran’s 13% would create a dangerous over-reliance on Moscow for a Beijing already seeking to replace the 4% of crude it imported from Venezuela. That over-reliance is likely to spur even greater Chinese efforts to achieve energy self-sufficiency via the electrification of its transport and manufacturing base, with implications for European manufacturers unable to compete with Chinese subsidies and production practices.

Conclusion

It is important to emphasise that many Gulf countries are almost entirely reliant on shipping (and air) transport for the provision of day-to-day goods, including FMCG and fresh veg. As the shut-down of the Strait continues, there is a real possibility of scarcity in those countries.

Whilst the global focus has been on the impact of the Iran war on oil and gas, there are second-order impacts which in the medium to long-term will be equally important. The longer-term impact is likely to result in weaker economic growth around the world – just as the Qatari Energy Minister has warned today.

I rather suspect that we are still very much only in the foothills of the consequences and impacts of this crisis. And the longer the Strait remains shut, the worse those effects are likely to become and the greater the pressure on the US to declare victory and cease the military campaign. It is a question of whose will is greater: Iran’s to survive; or the US’ ability to bear the economic pain.